ACA Status for New Full-Time Hires in the Gap Period

By Brian Gilmore | Published April 19, 2019

Question: How does an ALE determine the ACA status of a new full-time hire who experiences a reduction in hours prior to reaching a stability period under the look-back measurement method?

Compliance Team Response:

Reminder: Very Different Approach Depending on Measurement Method

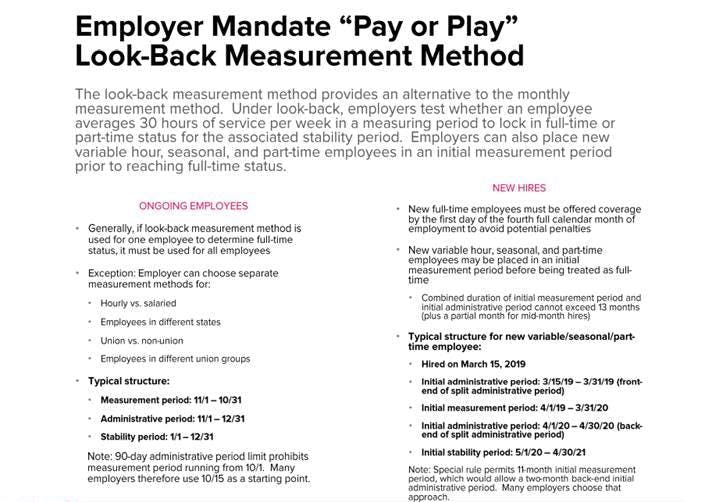

There are two different approaches for an applicable large employer (ALE) subject to the ACA employer mandate pay or play rules to determine employees’ full-time status:

The monthly measurement method; or

The look-back measurement method.

In general, employers with primarily full-time eligible workforces are best suited for the monthly measurement method. Employers with employees whose hours fluctuate above and below 30 hours of service per week will generally rely on the look-back measurement method because it provides greater predictability and stability for those workforces.

The measurement, administrative, and stability periods are relevant only to the look-back measurement method. They do not apply to the monthly measurement method.

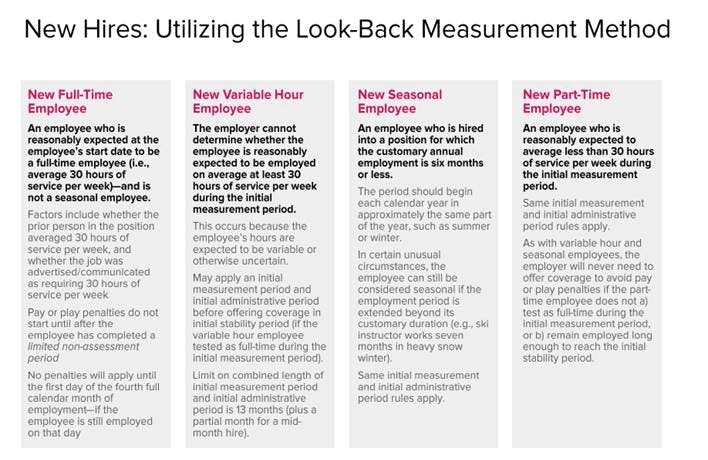

General Rule: New Full-Time Hires Under the Look-Back Measurement Method

A new hire who is reasonably expected at the employee’s start date to be a full-time employee (i.e., average at least 30 hours of service per week), and is not a seasonal employee, is considered a new full-time employee. Factors include whether the prior person in the position averaged 30+ hours of service per week, and whether the job was advertised/communicated as requiring 30 hours of service per week.

For new full-time hires, employers must offer coverage that is effective no later than the first day of the fourth full calendar month of employment to avoid potential ACA employer mandate pay or play penalties. There is no initial measurement period for new full-time hires. Such new hires will need to be offered an “effective opportunity to elect to enroll” in coverage sufficiently in advance of that effective date for the offer of coverage to be valid.

The Gap Period: New Full-Time Hires Prior to Reaching Stability Period

New full-time hires will not reach a stability period until they have completed the full standard measurement period (and the associated administrative period) that applies to ongoing employees. This will leave a long gap period (of potentially greater than two years) before there is a determination of the new hire’s ongoing full-time status for purposes of a stability period.

This “gap period” therefore represents the period between a new full-time employee’s date of hire and the start of the first stability period that applies to the new full-time hire.

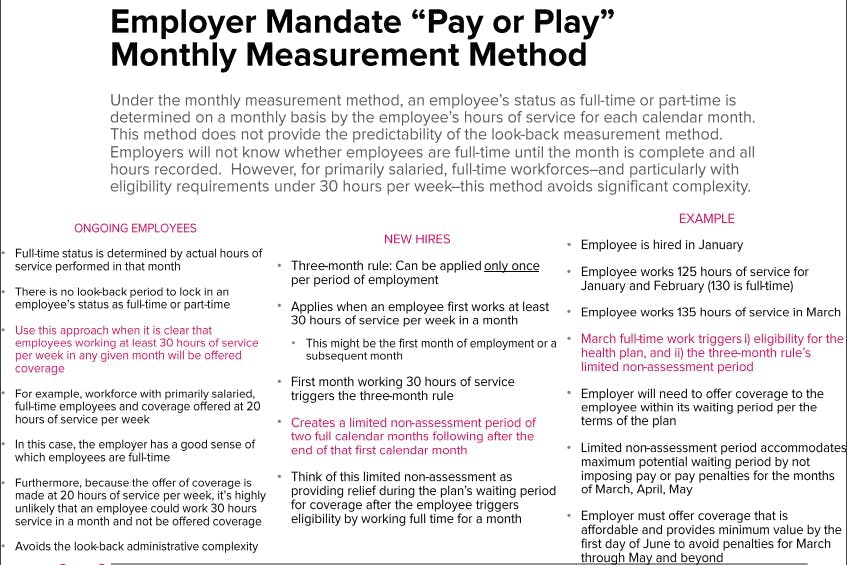

During that gap period before the new hire reaches a stability period, the employer uses an approach equivalent to the monthly measurement method to determine the employee’s full-time status. The employer will therefore determine the employee’s full-time status on a monthly basis based on whether the employee completed at least 130 hours of service in any given calendar month.

In other words, although the employer is initially required to offer coverage no later than the first day of the fourth full calendar month of employment based on the employee’s projected full-time status to avoid potential ACA employer mandate pay or play penalties, the employer is not required to continue offering coverage until the new hire completes a full standard measurement period for ongoing employees and eventually reaches a stability period.

During that gap period, the employee can lose full-time status by failing to complete at least 130 hours of service in any given calendar month. The employer is not required to offer coverage for any such month to avoid potential ACA employer mandate pay or play penalties because the employee is treated as part-time for any such month.

Once the new hire completes the standard measurement period for ongoing employees, the employee’s full-time status is determined exclusively by the measurement period results for the associated stability period in the same manner as all other ongoing employees.

Summary

Employers that utilize the look-back measurement method must offer coverage to new full-time hires that is effective no later than the first day of the fourth full calendar month of employment to avoid potential ACA employer mandate penalties.

The gap period between the employer’s initial offer of coverage to the new full-time hire and the employee’s completion of a full standard measurement period represents a tricky “gap period” for determining the employee’s full-time status prior to reaching a stability period.

During that gap period, employers will use the same approach as the monthly measurement method to determine the new hire’s full-time status. This means the employee will be full-time for any calendar month in which he or she completes at least 130 hours of service.

Once the employee completes a standard measurement period, the employee’s full-time status is determined in the same manner as any other ongoing employee. In other words, the employer will determine the employee’s full-time status for the stability period based exclusively on the employee’s hours of service completed in the immediately preceding standard measurement period.

More Information Regarding ACA Employer Mandate Full-Time Status Issues

Other Newfront Compliance FASTs discussing ACA employer mandate full-time status issues include:

Change in Employment Status During the Initial Measurement Period

New Hire Bona Fide Orientation Period Interaction with ACA Employer Mandate

ACA Employer Mandate Does Not Apply to Properly Classified Independent Contractors

Regulations

Treas. Reg. §54.4980H-3(d)(2):

(2) New non-variable hour, new non-seasonal and new non-part-time employees.

(i) In general. For a new employee who is reasonably expected at the employee’s start date to be a full-time employee (and is not a seasonal employee), an applicable large employer member determines such employee’s status as a full-time employee based on the employee’s hours of service for each calendar month. If the employee’s hours of service for the calendar month equal or exceed an average of 30 hours of service per week, the employee is a full-time employee for that calendar month. Once a new employee who is reasonably expected at the employee’s start date to be a full-time employee (and is not a seasonal employee) becomes an ongoing employee, the rules set forth in paragraph (d)(1) of this section apply for determining full-time employee status.

ii) Factors for determining full-time employee status. Whether an employer’s determination that a new employee (who is not a seasonal employee) is a full-time employee or is not a full-time employee is reasonable is based on the facts and circumstances at the employee’s start date. Factors to consider in determining whether a new employee who is not a seasonal employee is reasonably expected at the employee’s start date to be a full-time employee include, but are not limited to, whether the employee is replacing an employee who was (or was not) a full-time employee, the extent to which hours of service of ongoing employees in the same or comparable positions have varied above and below an average of 30 hours of service per week during recent measurement periods, and whether the job was advertised, or otherwise communicated to the new hire or otherwise documented (for example, through a contract or job description), as requiring hours of service that would average 30 (or more) hours of service per week or less than 30 hours of service per week. In all cases, no single factor is determinative. An educational organization employer cannot take into account the potential for, or likelihood of, an employment break period in determining its expectation of future hours of service.

(iii) Application of section 4980H to initial full three calendar months of employment. Notwithstanding paragraph (d)(2)(i) of this section, with respect to an employee who is reasonably expected at his or her start date to be a full-time employee (and is not a seasonal employee), the employer will not be subject to an assessable payment under section 4980H(a) for any calendar month of the three-month period beginning with the first day of the first full calendar month of employment if, for the calendar month, the employee is otherwise eligible for an offer of coverage under a group health plan of the employer, provided that the employee is offered coverage by the employer no later than the first day of the fourth full calendar month of employment if the employee is still employed on that day. If the offer of coverage for which the employee is otherwise eligible during the first three full calendar months of employment, and which the employee actually is offered by the first day of the fourth month if still employed, provides minimum value, the employer also will not be subject to an assessable payment under section 4980H(b) with respect to that employee for the first three full calendar months of employment. For purposes of this paragraph (d)(2)(iii), an employee is otherwise eligible to be offered coverage under a group health plan for a calendar month if, pursuant to the terms of the plan as in effect for that calendar month, the employee meets all conditions to be offered coverage under the plan for that calendar month, other than the completion of a waiting period, within the meaning of §54.9801-2.

Newfront ACA Employer Mandate Pay or Play and ACA Reporting Guide

Pay or Play Look-Back Measurement Method

New Hires Look-Back Measurement Method

Employer Mandate Pay or Play Monthly Measurement Method

Brian Gilmore

Lead Benefits Counsel, VP, Newfront

Brian Gilmore is the Lead Benefits Counsel at Newfront. He assists clients on a wide variety of employee benefits compliance issues. The primary areas of his practice include ERISA, ACA, COBRA, HIPAA, Section 125 Cafeteria Plans, and 401(k) plans. Brian also presents regularly at trade events and in webinars on current hot topics in employee benefits law.

Connect on LinkedIn